Industrial Valve Revenues Will Rise To Between $65 – $75 Billion By 2020

In 2014, Industrial valve sales were less than $57 billion. By 2020, revenues will rise to between $65 - $75 billion, according to the latest forecast from the McIlvaine Company in Industrial Valves: World Market.

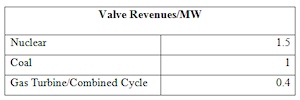

Inability to precisely predict revenues is due not only to the obvious factors such as general economic and population growth, but to variables in the process options. Valve investments vary from option to option. Using power generation as an example - if coal is considered as the basis for valve purchases, nuclear purchases of valves will be higher and gas turbines lower.

Efforts by environmentalists to reduce reliance on coal are falling on deaf ears in Asia. The cost and safety concerns about nuclear power are under scrutiny. Gas turbine revenues are going to rise at a faster rate than other options but from a relatively small base. It would take large double-digit gains to offset the valve purchases for other options.

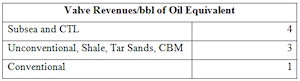

The biggest variable presently affecting valve revenues is the choice of oil and gas extraction method. There are large differences in valve revenues depending on the choice.

The price of oil has been cut in half from highs in 2014 of over $100/barrel. An increase in conventional production at the expense of subsea and other unconventional options would result in smaller valve revenues.

Valve sales for oil and gas will be negatively impacted by the lower prices. The question is: What is the magnitude and duration? Oil prices have always cycled. When prices fall, the highest cost producers cease activity. Ultimately, this creates shortages and prices rise.

Producers who will drop out in the short-term are operating on the following realities:

Exploration has been estimated to be around $30/bbl for a new source. So at $50/barrel, the exploration is going to drop substantially. However, exploration accounts for a relatively small percentage of the total valve revenues. Development includes drilling new wells in areas which have already been explored. So at $50/barrel, there will be justification for this investment. The cost of operating existing wells is small. Thus this production is unaffected.

The decline rate is the key factor in the rebound of prices and valve revenues. Averages of 10-15%/yr. have been cited for the industry. If no new wells were drilled, the flow would drop by 20 or 30% within just two years. The decline rate for shale sources in the U.S. is being debated. The ability of conventional suppliers in the Middle East to raise production from existing wells is also in question.

It is likely that demand will continue to rise. The lower oil prices and booming economies in Asia and the U.S. will contribute to that rise. So imbalances in supply/demand and potential shortages will lead to the next round of oil price increases and investment in unconventional sources.

Valve revenues will also be impacted by technology developments. The cost of direct coal-to-liquids could be as low as $40/barrel. If so, China would dominate the world energy picture. There are continuing developments in the extraction of oil and gas from shale. The cost of unconventional extraction rises as old wells need enhanced recovery, artificial lifts and other investments. As the cost of unconventional extraction is reduced, the margin between the two is narrowed. The result is less ability to manipulate prices by conventional producers.

Valve performance improvements are another factor which would positively impact valve revenues. There are lots of problems with subsea valves. Operators will be willing to pay more for valves which are more reliable under the most extreme conditions.

Other industries purchasing valves will be positively impacted by lower oil prices. So in the longer term, a decline in oil and gas valve revenues will be offset by gains in the chemical, steel, mining and other industries. The picture changes continually. McIlvaine revises its long-term forecasts at least once every quarter and more often if events so dictate.